It’s tough being an academic these days. Between the tiny number of permanent positions and the systemic exploitation of cheap labour, people are looking for a way out. Students, postdocs, and even PIs are asking themselves: should I join a startup? Should I make my own startup? It sounds seductive—change the world! Make money! Keep doing research, but in a less toxic environment! Who wouldn’t want to jump in at the chance of working on something innovative and useful?

People often ask me about my thoughts on industry: after my PhD and postdoc, I’ve worked in industrial R&D at big tech companies [Meta, Google], I’ve founded a medtech startup, I run a consulting business [xcorr.dev], I advise and have equity in early-stage startups [Artificio], I was the founding CTO for an education non-profit [Neuromatch]. Having experienced all these things, I want to take a step back to write this long note, so that you may learn from my tribulations.

There’s a lot of misleading information out there in the popular media: startups are depicted as exciting places where innovative research takes place outside the constraints of academia. I want to reset expectations and in particular explain how money flows in a startup. Startups lose money, at least for a while, and if they don’t figure out how to make money soon enough, they will go broke. Most PhD students & many postdocs are isolated from the $ and ¢ aspects of running a lab, and academics sometimes express disdain at commercialism. However, for-profit startups, are, well, for-profit, and they need cash to keep going. If startup life appeals to you, you need to understand the money flow.

This is particularly important to understand the role of research in a startup. You may ask yourself: will I be able to do research if I join startup X? The answer is: it depends. I end with a checklist of things you might want to consider before you decide to dedicate multiple years of your life to a startup.

Subscribe to xcorr and be the first to know when there’s a new post

What’s a startup anyway?

A startup is a newly existing business that seeks to scale a given business model. For example, let’s say you have an idea for a new widget and you do market research to show people will buy said widgets. You may then convince investors to give you money to create a widget factory and start selling widgets. Congratulations! You have a startup.

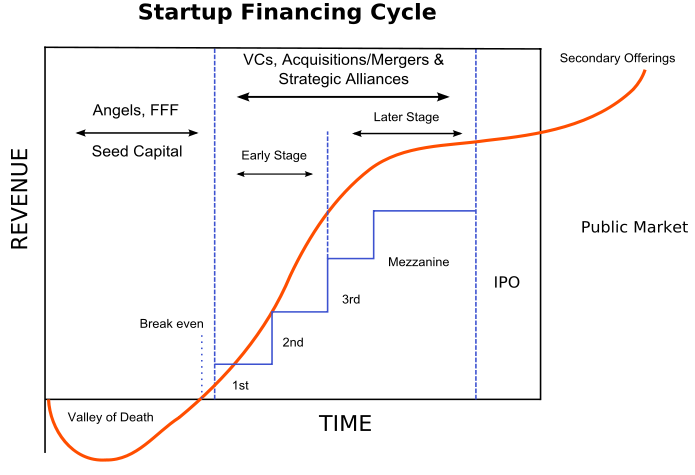

Startups often start by losing money on salaries, capital expenditures (i.e. stuff like servers, factories, and so forth), lawyer fees, etc. This is known as the valley of death. Many startups are default-dead: to continue operating, they have to replenish their coffers with a constant influx of capital from external sources. These investments are conventionally structured in rounds, occurring every 12-18 months, starting with a pre-seed round, then going on to a seed round. Starting from series A onwards, startups often display revenue, though not enough to fund their massive expansion. Scaling is often necessary to make a startup ultimately profitable–a widget factory might cost the same regardless of whether it produces 1,000 widgets or a million. Therefore, by selling lots and lots of widgets, you spread the fixed cost of the widget factory over many widgets.

Startups’ long-term trajectory can be one of:

- run out of money and close down

- get acquired

- become public companies

- remain private for a long time, for various strategic reasons

To raise money, they sell off chunks of themselves to investors. Doing so dilutes the ownership of the original owners. Instead of owning 100% of my business, if I sell off 20% for a chunk of change (say, 200k$), then my business is valued 1M$ and I own 80% of it. Dilutive funding is often offered by venture capitalists (VC). Non-dilutive funding, which doesn’t cost any ownership, is done by government orgs (e.g. the NSF, various agencies in Canada, etc.).

Importantly, most startups don’t succeed – the general rule of thumb is that out 10 startups that receive seed investment, 7 will close down, 2 will break even, and only 1 will see a significant return on investment to the investor.

What determines a startup’s value?

Startups survive by selling chunks of themselves to investors. How do you value a chunk of a startup?

If I try to buy the poutine stand down the street to become a restaurateur, there’s a few well-established ways to price that: I might look at the price of poutines they sell a year (gross income), or their net income, that is, poutine sales minus salaries minus other expenditures. Then I could apply a multiplier to get a ballpark valuation number. If the industry-wide revenue multiple for an independent restaurant is .3, and they’re selling 300k$ worth of poutine a year, a smooth 45k$ might get me into the restaurant business.

But multipliers don’t work if a startup is making no money! You might be asking: how can you ask people for money to own something that makes no money? How is it that the poutine stand down the street—bringing real value to the people in the form of delicious carbs—can be bought for less than the price of a Tesla, while a guy with a half-baked idea and no sales can value his startup at 3M$?

One method to value a startup is the so-called VC method. It states that the value of a startup is some discount factor for risk times the expected value of the business at some time in the future (say, 5 years). Let’s look at each of these in turn.

- Discount factor for risk: If I’m willing to take no risk at all, I can put money in high-savings rate account and make about 3% per year in these days of high interest rates. Free money! If I can afford a little risk, I can put money in an index fund and make an average of 8% a year, with some variance. Higher risk tolerance is rewarded with higher average returns. When an investor puts money in a startup, with a >50% risk of losing all of it, they will require much higher multipliers for it to be worth it—perhaps on the order of 50% year-on-year. The total discount factor is equal to (1+d)^-X, where X is the number of years at maturity (say, X = 5)

- Future value of the business: that can be estimated using the same type of calculation used to estimate the value of a poutine stand. Tech businesses have much higher multipliers (aka price-to-earnings) than brick-and-mortar independent restaurants: the industry average is 20. Thus, if your business could be making 10M$ in annual sales in 5 years, according to this calculation, it would be worth 200M$.

I like to think about the discount factor in a slightly different way: I like to think about it in terms of p(things will work in X years). Hence, the value is:

Note: this is a highly simplified model, and doesn’t take into account that you may have several sales scenarios, each weighted by their likelihood, etc. The lessons are broadly the same regardless of your exact valuation model.

Generally, you’ll want each successive funding round to be at a valuation of 2–3X higher than the last one, otherwise you will quickly dilute yourself out of a business. Investors also hate so-called down rounds, where the startup is valued less than previously, because that means that they overpaid for their investment. Sometimes a miracle happens and you discover more yearly sales—equivalently, a larger total addressable market—prior to starting to sell things, but that is a very rare occurrence indeed. That means that the only thing you can really work on to increase the value of your startup and survive to live another day is to make your product or business “more certain to work” by a factor of 2–3X every 18–24 months. In other words: you should work to decrease risk.

What kinds of risks do startups face?

So far we’ve established that decreasing risk is a key activity in a startup. What kinds of risk are we talking about anyway?

Market risks

Will people want to buy the thing you’re selling at a price that will ultimately make you a profit? Generally, investors don’t like to invest in widget businesses where it’s not very clear whether anybody will buy the widget. You can address market risk by:

- Showing that you already have sales. Definitely the best. If you have 100 clients willing to buy a thing at a decent price and you’re growing year-on-year by 10X, then it won’t be too hard for an investor to believe you have a viable business.

- Showing that people are using the thing and they like it. Maybe you haven’t figured out how to sell a widget, but you might be able to show that people use a free, minimalistic version of a thing (MVP) and love it. That can mean having alpha users or demo installs.

- Showing that people will actually buy the thing once it’s made. That can mean getting a letter-of-intent from some big client saying they’ll buy the widget once it’s made.

In all these cases, you need to build things. It’s hard to get a letter of intent for something you can’t hold in your hand in a prototypical manner. To decrease market risk, you have to build a prototype and then a minimum viable product (MVP).

Technological risk

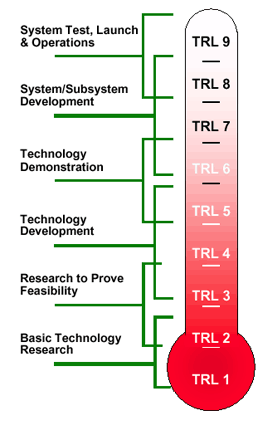

Perhaps the product you are building is based on a principle that has been demonstrated only on a small scale in a lab, or maybe even just on paper. The usual scale to establish the technological maturity of an idea is TRL (technological readiness level). It comes from NASA’s classification system to judge prospective technologies for use in space, but it’s been broadly adopted in early stage R&D. The higher the TRL, the lower the risk.

Early-stage, pre-revenue startups will need very deep pockets to work on ideas at TRL1—TRL2. That really only makes sense if the market is so obviously large (”blockbuster”) that the risk and time expense can make sense. Maybe somebody will fund a TRL1 nuclear fusion startup, because clean energy at scale is such a large market. Otherwise, TRL1—2 is usually done at research institutions with public money, with the outcome, knowledge, becoming a public good. Early-stage deep-tech startups typically focus on TRL3—6 instead.

Building an MVP can really decrease technological risk because it shows the thing actually exists. Generally it’s a bad idea to combine something that has high technological risk with high market risk. A better combo might be: show that something has a big, obvious addressable market if only this very difficult technological/science problem can be overcome by the world’s foremost expert in this area, who happens to be you. Or maybe you have already built a super special, super cool technology and you think, I think maybe somebody would buy this, but you need to do market research.

Aside & rant: it can be a pointless exercise to try to forecast how basic research ideas done at research institutions will translate into tangible, marketable goods, because there are so many steps between the research and its commercialization. That means that judging basic research based on commercialization potential (as funding agencies increasingly do) can be an exercise in futility. Fundamental research is better judged by criteria such as: is this interesting?

Regulatory and IP risk

If you do anything medical, much of the uncertainty will be regulatory. Is your medical device class II or class III? The burden of proof and the cost of trials in each case will be different. Do you have access to the necessary intellectual property (IP)? Can you protect yourself long enough to go to market without somebody doing the thing you were planning to do eating your lunch?

Execution risk

Sometimes all the stars are aligned: the market is there, the innovation works, you’re lawyered up, but you still fail to deliver a good product. Maybe you don’t hire the right people; people who are too research-y or insist on putting things which don’t work yet into production. You get into constant fights about priorities and every planning meeting is a mutiny. You get a lawsuit at an inopportune time. Many factors can converge to cause a good idea with a demonstrated market to fail if not executed properly.

If it’s too good to be true, it probably is

We hear a lot about “research-labs”-like startups that don’t have any visible products and that seem to be doing great. This sets a really bad precedent for students and postdocs, because it gives the impression that there’s some free money floating out there. If it looks too good to be true, it probably is.

We don’t hear so much about startups that fail, because dead men tell no tales: it’s similar to the file drawer problem in academia. We often hear of successful AI startups, but we seldom hear about the cautionary tale of ElementAI. ElementAI was a startup originated from Yoshua Bengio, Turing-award winning AI researcher. They used up a lot of money to bring AI-based solutions to businesses, but grew too fast without a laser-tight focus on a single, scaleable product that could be sold. The fact that it was started by somebody famous is completely irrelevant: it may have hurt them, because they were able to raise money too fast to get their feet solid and prove a product-market fit. At some point, the startup has to sell a product for more than the cost of the inputs to the product. In this case, they were sold for scraps, employee stock became worthless, and many wasted years of their lives in the debacle.

Understand the hypothesis underlying what a startup is doing and the addressable market. If it makes sense, jump in. If you cannot make the numbers add up and the people in the startup can’t give you a good story, you need to get out of there. I’ve heard students and postdocs tell me that they’re skeptical of startup X but want to jump in anyway, because, hey, what do they know? If you’re a subject domain expert, you often know more about the technology being developed and its risk profile than 90% of people involved. You should combine your pre-existing technical knowledge with knowledge about the market, which can be acquired pretty fast. If you do this, you can invest your time and energy on what you sincerely believe is a winner rather than engage in magical thinking.

What can you do as a PhD to help your startup succeed?

Now we get to the crux of my argument: your job, as a PhD in an early-stage startup, is to reduce risk. You have several ways of doing this:

- Helping to build an MVP or prototype

- Talking to people who will use the product to make it better (needs-driven design)

- Do research showing the efficacy of the product for its intended purpose

On this last point, you might think that industrial research is less reliable (sloppier) than academic research: if you have financial incentives to show something is true, wouldn’t you want to show that it’s true? In fact, you have every incentive for the research to be correct – not as in “finding the answer management wants to be true”, but as in “finding the right answer”. Finding the right answer decreases the inherent risk in the venture, which means you’re likely to survive another day: if the hypothesis underlying the startup is wrong, you should pivot now rather than later when you’ve burned through your cashflow.

Because a pre-revenue startup has so much uncertainty and doesn’t have the cash flow to cushion the blows, you should be working on little R research. I would also argue that you should deeply understand the market at this point, and avoid doing R&D fenced off from the business: your research needs to translate pretty quick into things people can buy, ideally within one round of financing (18–24 months).

Papers, what are they good for?

Publishing papers in this environment is a mixed bag. Positive incentives to publish include:

- researchers want papers, and keeping high-value researchers happy is often a primary incentive for the startup, as employee churn is expensive.

- the research itself can bring value to the company by decreasing uncertainty and reorienting activities depending on findings.

- the seal of approval from peer-reviewed research can reassure investors the work is innovative in ways and uncertainty has been decreased. Be careful though, ultimately, it’s not hard for an investor to find an expert senior postdoc and give them several hundreds of dollars to thoroughly review your claims. That due diligence is any many ways far more extensive than peer review ever could be.

- recruiting high-value researchers can become easier if they have visibility into the research the company does. That’s also one reason many startups have company blogs.

- research may be required to pass regulatory hurdles, for example with medical devices.

However, there are many downsides:

- papers don’t pay the bills: clients do. Papers can be a huge distraction and encourage scientists to isolate themselves from the business and not contribute to product early on.

- research creates intellectual property, which brings value to the company; but publishing that IP prevents patenting. It allows competitors to copy the innovation.

In conclusion: an early-stage startup that doesn’t seem to have many clients but has a lot of papers coming out is usually a warning sign. As a large shareholder in a startup, or an early employee in charge of R&D, you have to make sure you do the right kinds of research, and create a culture that incentivizes the continued existence of said startup.

Later-stage startups and companies with mature cashflows are in a better position to engage in big R research. Even then, however, the goal is rarely the production of knowledge, understood as a public good–though on occasion good PR could be valuable for secondary purposes like recruiting. The purpose instead is to perform research in such a way that ultimately feed into new products down the line that translate into sizeable revenue. Companies with long runways–for instance Meta with its Metaverse strategy–can afford to use a very long horizon to evaluate research. However, that’s only viable because Meta has tens of billions of dollars in cash reserves AND a positive cashflow. Most startups and companies are not in that case.

How not to succeed as a startup

You can learn from my mistakes. I was briefly the CTO of a medtech startup that used AI to treat a given neurological condition. As a PhD, it was my job to decrease the uncertainty surrounding the startup rapidly for us to raise money. I did all the activities expected of that role: created valuable IP that could be protected, did studies demonstrating our proof-of-concept, participated in product development, etc.

However, in doing so, I isolated myself from the marketing and fundraising aspects of the startups. What I should have focused more on was validating the market. Digging deeper and deeper, we realized that the market we had hoped for was smaller than anticipated as we uncovered a number of contraindications for the treatment we were building. To address a larger market through a different indication would have increased the uncertainty about efficacy to an unacceptable level. Ultimately, without a sizeable market, the opportunity was dead in the water. Although we could have continued to grind things out for a number of years, because the market opportunity was so small, it seemed a better trade-off to shut things down. A couple of papers and a patent are simply pointless for a startup unless you can turn that R&D into something that can ultimately be sold.

What about my favourite R&D startup?

I’ve shared my thoughts on the role of research in a for-profit startup with many over the years. I inevitably get pushback, often in the form of “what about startup X? It looks like they’re just doing R&D and doing fine?” Let’s deconstruct some counterexamples that people frequently cite.

Disclaimer: although I worked at Facebook and Google, I don’t have any special insight about these startups that were ultimately acquired by Facebook and Google, I’m just reading the publicly available information.

Deepmind

Deepmind, the artificial-general-intelligence company, is an interesting case. It was acquired in 2014 by Google at a reported 600M$. At the time, they had about 75 employees. For a company that had no visible product, its exit paths were rather narrow: an early investor confided that had they not been acquired by Google, they would have probably failed. About 8M$ per employee is pretty expensive for an acquihire, but if you look at contemporary discussions on HackerNews, commenters speculate that the core value of the company was indeed its people: recruit AI researchers cheaply in Europe, repackage as a functioning R&D team that could be sold to a tech giant. That would make Deepmind prior to its acquisition, in essence, a recruiter specialized in AI talent.

Compared to other acquisitions around the same time, it was cheap: WhatsApp was acquired the same year for 19B$, with 55 employees at the time, that would come with about 40X the price per employee. I don’t want to imply that Deepmind’s sale to Google was a firesale. However, in my mind, its sale was not the roaring success that some claim it was. Deepmind’s path was quite narrow, and I don’t think it’s replicable today.

Ctrl-Labs

Ctrl-Labs built neural interfaces for AR/VR. They assembled an R&D team to create a neural interface that detect the smallest of neural impulse close to the wrist and translate that into commands to a computer. At the time of acquisition, they were–to the best of my ability to search through the internet wayback machine–a pretty small team, perhaps on the order of a dozen people. They were acquired by Facebook in 2019 for a reported 500M$-1B$. Importantly, however, they had real protected intellectual property – a portfolio of their own patents plus IP acquired from North (previously named Myo). Their R&D had been translated to a real prototype, which they presented at conferences. They had a real use case, which is interfacing for AR/VR. In other words, they had removed much of the technical uncertainty around the technology, in precisely the way I’m advocating here. In my view, it’s a good example of the role of R&D is in an early stage startup.

FROs & OpenAI

So far our discussion has been focused on for-profit startups, which are by the far the most common legal structure for what we call “startups”, and which have the constraints that I discussed previously. People are actively looking for different legal structures that allow them to do big-R research outside the confines of academia.

Focused Research Organizations (FROs) are a new kind of model that’s emerging that’s potentially very exciting. They focus on building one highly specific public good (e.g. a tool, a dataset) that they can deliver within a time frame of ~5 years. Importantly, most FROs are non-profit organizations, and funders understand that the effort is oriented towards this specific outcome without the expectation of profit. They’re very much an experiment at this point, but it will be interesting to see what comes out them.

Another example of an alternative model is OpenAI. OpenAI was started as a non-profit with a billion dollars in funding, and received a further injection of 1B$ from Microsoft following its re-incorporation as a limited-profit company. Much of their research is done out in the open (although GPT-3 and DALL-E2 checkpoints have not been released). Notice, however, that despite its legal status, OpenAI does have revenue through GPT-3. Indeed, non-profits or limited-profits still need to have a valid business model or constant cash influx to continue operating.

Perhaps a specific FRO’s cash flow looks like “we have exactly 30M$ from a donor to create a new tool, then we will release the tool and then shut down”. As long as everybody knows what they’re getting into, I applaud these efforts at finding alternatives. However, for startups incorporated as for-profits, which is the vast majority of startups, doing blue-sky research un-anchored to a product is a sure-fire recipe to run out of cash.

A checklist for joining a startup

If you’re thinking of joining a startup, ask yourselves these questions:

- Is the thing the startup working on necessary? Does anybody actually care?

- Is this a cool, innovative product?

- Do I think it’s doable, technically?

- Do I think that people are going to buy the thing the startup sells?

- Will I have the agency to positively affect the course of the startup?

- How much can I grow as a scientist/programmer/data scientist within the group?

- What do I think about the people that run this startup? Do they know what they’re doing? If it’s their first time, are they getting the mentorship they need?

- Do they have money? How much? Where are they in their fundraising?

- Will I be able to do the kinds of research I want to do? Little R research? Big R research? Product dev?

- Are there any other red flags? Have several people asked “I don’t understand, how can they stay in business?” Is one of the founders a creep or a cult leader or has anger-management issues?

Conclusion

A startup’s goal is to make money back to its investors by using a scalable business model. In an early stage startup, it is very rare that your job will be to “do research and publish papers”. Publishing papers can, in some circumstances, increase the value of the startup and keep it afloat, but much of the time it can be a distraction unless it’s aligned to business goals. Technical staff should understand these business goals and align to them. R&D cannot be separated from the business until the startup is post-revenue and on more solid footing.

{kind=link}

4 responses to “How science startups actually work”

[…] https://xcorr.net/2022/11/03/how-do-science-startups-actually-work/ […]

Spend enough time on the money question to convince yourself that they are likely to last long enough for you to meet your personal goals. Startups die when they run out of cash. Understand their cash flow plan and carefully consider any plans to raise money. You will have to ask questions; be polite but thorough.

Nice article, Patrick.

Amazing post and relevant to me. Can you talk about Anthropic? they raised 700M$ with no visible business plan.

A very useful article, Patrick! Thanks for posting it.

I’m wondering whether startups have internship programs. If yes, do you think getting into the startup of interest as an intern (while one is still in the PhD program) would be a better way to get an idea about research/opportunities?

Or, it’s better to intern in an already well-established company?